Why This Article Matters

The AI banking solutions market has a structural problem that no one is naming clearly: solutions are evaluated on the dimensions where they are all strong, and purchased on terms that do not predict the dimension that actually matters – production reliability at 6, 12, and 18 months. This article names the incentive structure that produces untrustworthy solutions, describes four failure patterns that repeat across institutions after deployment, and delivers five specific questions that change the evaluation from capability assessment to trust qualification. These questions are designed to be used directly in procurement conversations. A vendor who cannot answer them specifically has not built for production.

Why the Market Systematically Produces Untrustworthy Solutions

The AI banking solutions market is thriving. Every major capability gap has a solution ecosystem. Vendors with sophisticated technology, credible reference clients, impressive benchmark results, and compelling demonstrations.

The problem is not the market’s size or ambition. It is the evaluation framework most institutions are using to navigate it.

AI banking solutions are evaluated on capability: what the solution can do, how accurately it performs, how quickly it processes decisions, how readily it integrates with the stated architecture. These are the wrong evaluation criteria – not because capability does not matter, but because capability is the dimension on which every serious solution performs adequately. It is not the dimension on which they diverge.

The dimension on which solutions diverge, consistently and consequentially, is production reliability – the ability to perform consistently under real-world data conditions, to maintain that performance as the environment around them evolves, and to do so within governance boundaries that satisfy the regulatory obligations of the institution deploying them.

Understanding why the market produces this pattern: vendors are incentivised to win deployments, deployments are won by capability demonstrations, and capability demonstrations are conducted under conditions the vendor controls. Institutions are incentivised to complete deployments – deployment milestones drive programme reporting, programme reporting drives executive confidence. The KPIs that govern transformation programmes measure go-lives and automation rates – not the production reliability of what went live at month 12.

What an AI Banking Solution Actually Is

An AI banking solution is not a model. It is not an application. It is a composite system – an interconnected set of components that must all function correctly, and function correctly together, for the solution to deliver reliable outcomes in production.

The composite system comprises four layers that map directly onto the Four-Layer Trust Architecture:

- The data layer: – the pipelines, integration points, and data sources that feed the model. A state-of-the-art model on a poorly governed data layer is not a trustworthy solution. It is a high-performance engine running on inconsistent fuel.

- The intelligence layer: – the model itself, its inference logic, and the explainability infrastructure that surrounds it.

- The integration layer: – the connections between the solution and the core banking systems, digital channels, downstream workflows, and other AI systems it interacts with.

- The governance layer: – the compliance frameworks, audit trail mechanisms, monitoring infrastructure, and accountability processes that ensure the solution operates within regulatory boundaries.

A solution is only as trustworthy as its weakest layer. And the weakest layer is almost never the intelligence layer, where vendor demonstrations focus. It is almost always the data layer, the integration layer, or the governance layer – precisely the layers that demonstrations undertest, pilots under-pressure, and reference calls underreport.

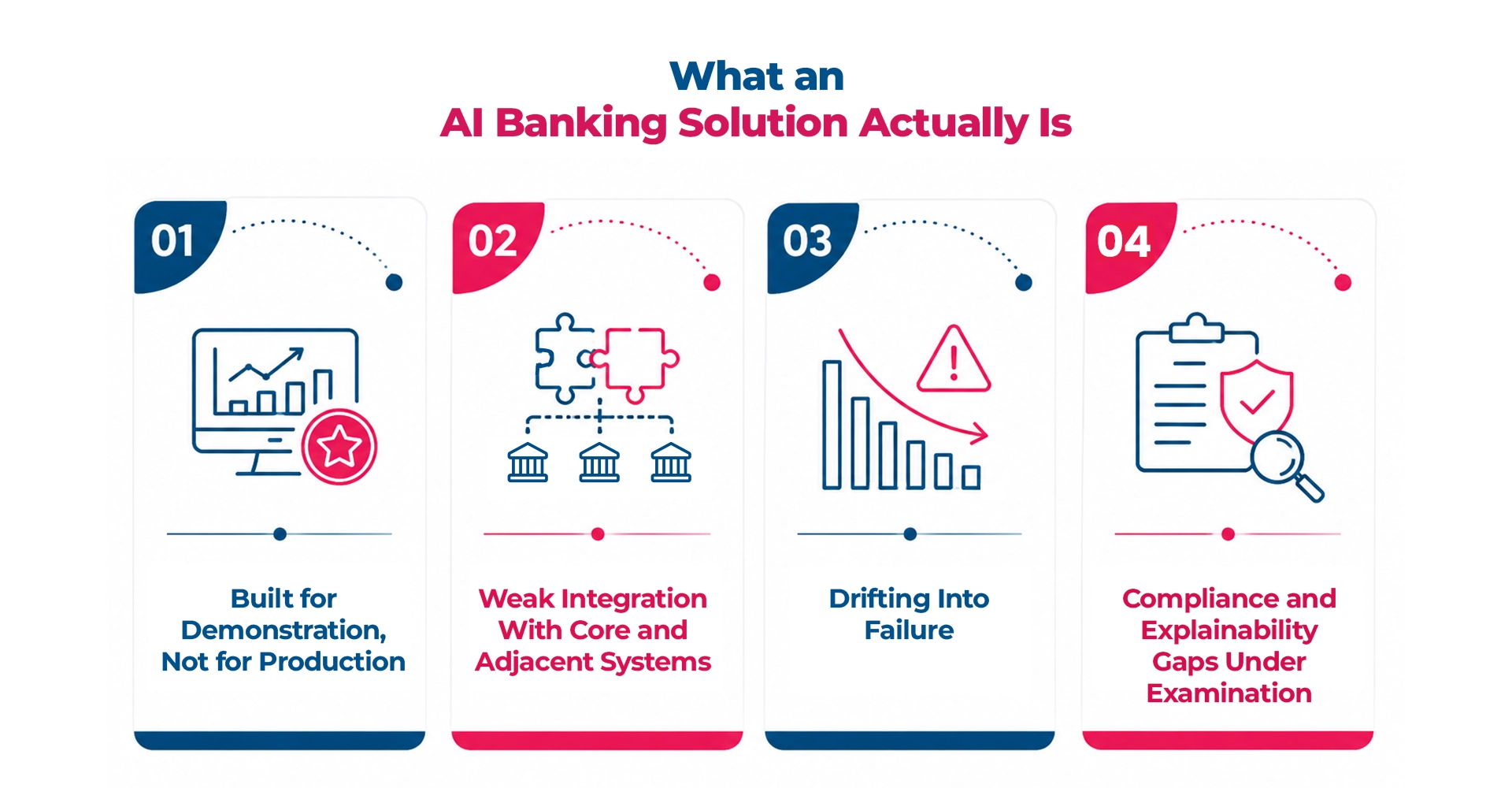

Four Production Failure Patterns

Pattern 1: Built for Demonstration, Not for Production

The most pervasive failure pattern is the fundamental mismatch between the environment in which the solution was designed and tested, and the environment in which it must actually perform. Production banking environments are characterised by data variability that curated demonstration data sets do not represent. The accuracy figure from the demonstration is not wrong. It is simply not predictive of production performance.

Pattern 2: Weak Integration With Core and Adjacent Systems

The solution is evaluated against a defined data interface specification. Over the twelve months following deployment, the core banking system undergoes a release that changes a field naming convention. A data migration project alters the customer master record format. None of these changes is made with intent to disrupt the AI solution. Each is made by a team with no visibility into the AI solution’s dependency on the specific data structure being changed. The AI solution’s behaviour change is not detected until a business process review three months later identifies a systematic decisioning anomaly.

Pattern 3: Drifting Into Failure

Model drift is the gradual divergence between a model’s production behaviour and its validated performance baseline. Every production AI model drifts. The question is not whether it drifts, but how quickly and whether the institution has monitoring to detect it before the drift has propagated into enough decisions to create a material problem.

Without continuous monitoring, drift is invisible. It accumulates silently in aggregate performance metrics that no one is tracking continuously – until it surfaces as a regulatory finding, a customer complaint pattern, or a business performance anomaly. The cost of discovering drift at this point is a multiple of the cost of detecting it early.

Pattern 4: Compliance and Explainability Gaps Under Examination

The fourth failure pattern has the most direct regulatory consequence – and is most systematically absent from vendor evaluation processes, because the regulatory examination that reveals it typically occurs 12 to 18 months after deployment, well outside the evaluation window.

Vendors demonstrate model accuracy. They do not typically demonstrate – because they are not asked to – whether the solution can produce a decision-level explanation for a specific adverse decision in the format and within the timeframe that a regulatory examination requires.

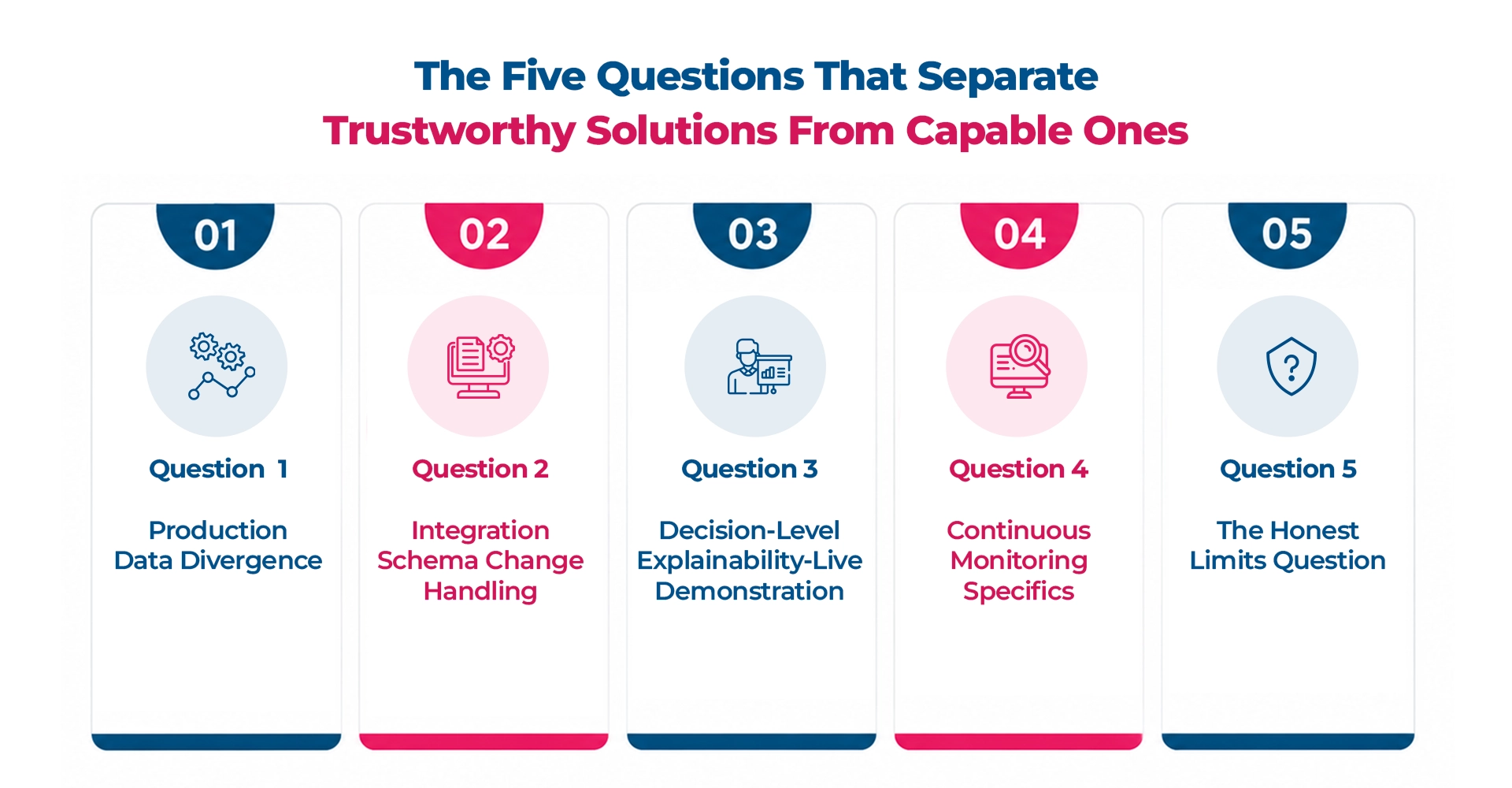

The Five Questions That Separate Trustworthy Solutions From Capable Ones

Question 1: Production Data Divergence

How does your solution perform when the data it receives in production differs materially from the data it was trained or configured on? The answer should name a specific live deployment where distributional shift occurred and describe what the monitoring detected. An answer that describes design intent without referencing live production evidence is incomplete.

Question 2: Integration Schema Change Handling

If one of the core systems your solution integrates with makes a change to its data schema, how does your solution detect that – and what is its behaviour in the period between the change and its detection? The answer should describe a specific data contract or integration monitoring mechanism, not a general statement about integration resilience.

Question 3: Decision-Level Explainability – Live Demonstration

For a regulated adverse decision made by your solution three months ago, walk us through – right now – how we produce a decision-level explanation. This question should be answered with a demonstration, not a description. If the answer is a description of the feature importance framework the model uses, decision-level explainability does not exist.

Question 4: Continuous Monitoring Specifics

What does your continuous monitoring cover, at what frequency, and who in our institution receives the output? The answer should be specific about metrics, specific about governance thresholds and who owns the response, and specific about what happens to monitoring continuity when the vendor relationship ends.

Question 5: The Honest Limits Question

Which decisions that your solution is capable of making should not, in your assessment, be made by AI without human review in a regulated banking environment – and why? A vendor who answers this with specificity – naming the decision categories where their solution’s limitations make direct AI decisioning inadvisable – is a vendor who understands the environment their solution operates in. A vendor who answers every use case with ‘yes, we can do that’ is a vendor whose governance thinking has not kept pace with their capability development.

The Evaluation Shift

The question is no longer: ‘What can this solution do?’

It is: ‘Can this solution be held accountable for what it does – consistently, over time, under the conditions of a live regulated banking environment?’ The market will not be defined by who built the most capable AI banking solutions. It will be defined by who built solutions that banking institutions can genuinely trust.

The full research report applies the trust qualification framework across the complete AI banking solutions landscape – including the composite system definition, the four-layer evaluation model, and how trust qualification connects to the broader Four-Layer Trust Architecture.

Download the Full Research Report: Engineering Trust in AI-First Banking

What to Read Next

PREVIOUS: Generative AI in Banking: Opportunity Without Control Is Risk

NEXT: AI-Enabled Core Banking: Re-Architecting the Foundation for Intelligence

This article is part of the Engineering Trust in AI-First Banking series, examining the framework that separates institutions that scale AI from those that stall.

FAQ

1. Why does the AI banking solutions market systematically produce untrustworthy outcomes?

The market is structured around capability demonstrations – accuracy benchmarks, feature lists, integration speed, vendor case studies. These are procurement signals that measure what a solution can do in optimal conditions, not whether it will perform reliably in the complexity of a live banking environment over time. Solutions optimised for sales cycles are not the same as solutions optimised for production reliability, and the gap between the two is where most AI banking deployments encounter their first serious failure.

2. What are the five evaluation questions that change how a bank selects an AI banking solution?

The five questions are: Does it perform in your specific data environment, not just in vendor benchmarks? What is the continuous monitoring and drift detection architecture, not just the deployment architecture? Can it produce an explanation for any individual decision on regulatory demand? How does it integrate with your existing data governance and audit infrastructure? And what does the vendor’s track record look like in environments of comparable regulatory complexity – not just comparable size?

3. How should banks evaluate AI vendors for trust and governance maturity, not just technical capability?

Evaluate governance maturity through the same lens as the Four-Layer Trust Architecture: ask specifically about how the vendor handles data lineage and input validation (Data Trust), continuous model monitoring in production (Model Trust), system reliability under banking-scale load and edge cases (System Trust), and the explainability infrastructure available for individual decision reconstruction (Outcome Trust). Vendors who answer fluently across all four layers have built for banking. Vendors who focus on capability and defer governance are optimised for the demonstration environment.

4. What is the hidden cost of deploying AI banking solutions that lack trust infrastructure?

The direct costs are remediation, model rollback, and regulatory penalty. The indirect costs are more significant: every AI system deployed without adequate governance adds to an institution’s trust debt – the accumulating gap between AI capability and the confidence infrastructure overseeing it. Trust debt is invisible until it is tested: by a production incident, a customer complaint that triggers regulatory scrutiny, or an examination that finds governance documentation that does not reflect operational reality. At that point, the cost of closing the gap is multiples of what building it correctly would have cost.

5. Can off-the-shelf AI banking solutions be made trustworthy, or does trust require custom-built infrastructure?

Off-the-shelf solutions can be deployed within a trustworthy architecture, but the architecture itself requires deliberate engineering – it cannot be assumed from the vendor. The trust infrastructure (data contracts, continuous monitoring, explainability pipelines, governance integration) typically needs to be established as a wrapper around deployed solutions, regardless of how capable those solutions are. Institutions that assume trust is a product feature they can procure consistently discover otherwise at the first production incident.