Why This Article Matters

Compliance is not simply another domain where AI creates opportunity and risk in equal measure. It is the domain where the quality of every other AI trust decision the institution has made – in data governance, model design, system architecture, and delivery governance – becomes visible, auditable, and actionable by regulators. This article makes the most important distinction in compliance AI: automation addresses volume, assurance addresses accountability. They are not the same thing – and the 88% of institutions deploying compliance AI without adequate governance are discovering that difference in examination findings. The three sequenced shifts described here are the path from one state to the other.

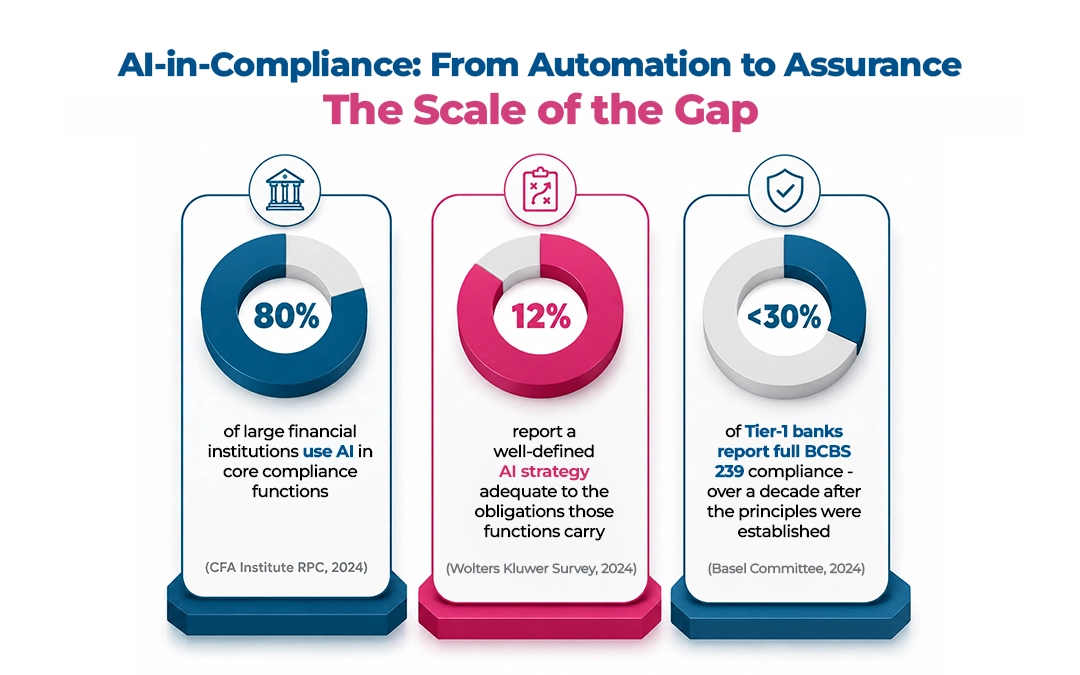

The Scale of the Gap

80% of large financial institutions use AI in core compliance functions (CFA Institute RPC, 2024)

12% report a well-defined AI strategy adequate to the obligations those functions carry (Wolters Kluwer Survey, 2024)

<30% of Tier-1 banks report full BCBS 239 compliance – over a decade after the principles were established (Basel Committee, 2024)

These numbers describe an industry that has automated compliance at scale without building the governance infrastructure that operating compliance AI in regulated contexts requires. The examination cycle is closing in on that gap from the outside while institutions are still trying to close it from the inside.

Automation Is Not the Same as Assurance

The instinct that drives AI adoption in compliance functions is correct: compliance obligations are growing faster than human compliance capacity. AI that automates these functions is not a luxury – in many institutions it is the only operationally viable path to meeting current obligations.

But automation and assurance are not the same thing. And the gap between them – between a compliance function that uses AI to process more work and one that uses AI to produce continuously defensible outcomes – is precisely where most institutions’ AI compliance programmes have stalled.

An automated transaction monitoring system that processes one million transactions per day and produces a manageable number of alerts has solved the volume problem. If those alerts cannot be explained to a regulator – if the system cannot reconstruct why transaction 847,293 was flagged and 847,294 was not, in a form that satisfies the examination standard – the assurance problem remains entirely unsolved, regardless of the processing volume.

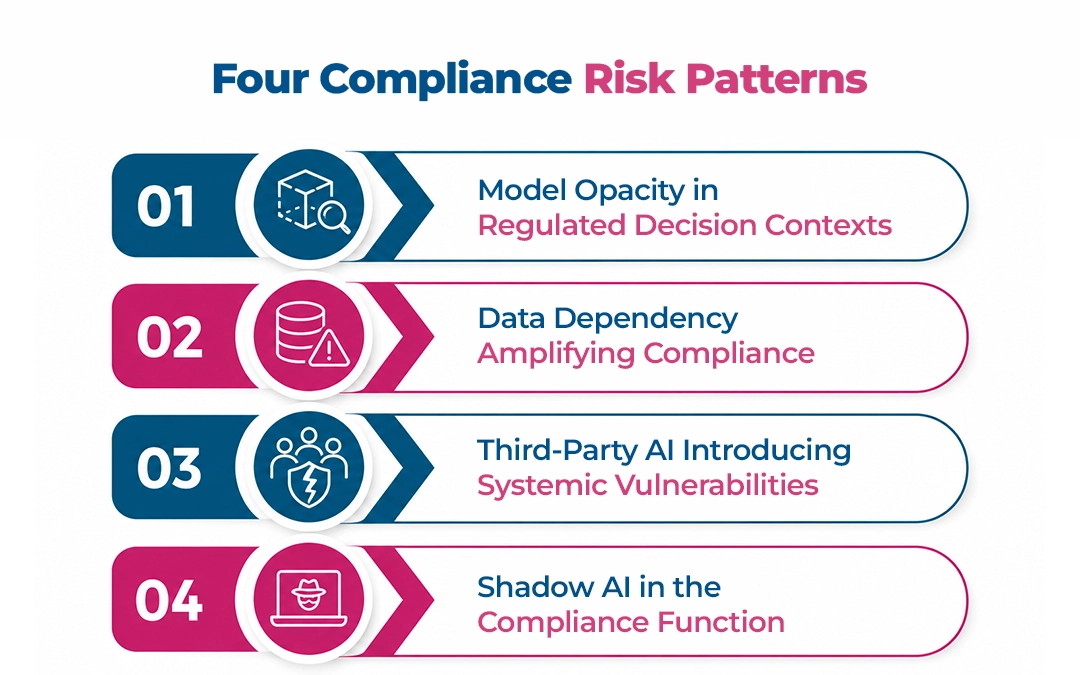

Four Compliance Risk Patterns

Pattern 1: Model Opacity in Regulated Decision Contexts

AML systems, credit compliance systems, conduct surveillance – these operate in the most heavily scrutinised decision contexts in any regulated industry. Each carries explanation obligations that exist regardless of the technology used. When a compliance AI system’s decision is challenged, the institution must provide a specific, coherent account of why that specific decision was made.

EVIDENCE

SR 11-7 – the Federal Reserve’s model risk management guidance – is explicit: vendor models require the same validation and ongoing oversight as internally developed models. A compliance AI programme substantially dependent on third-party models, governed only at the vendor level, has a model risk management gap that a supervisory examination will identify.

Pattern 2: Data Dependency Amplifying Compliance Exposure

Every compliance AI system is a data consumer. The quality of its decisions is bounded by the quality of the data it processes. In the compliance domain, data quality failures extend to the regulatory defensibility of the entire compliance programme – not just the accuracy of individual outputs.

BCBS 239 established more than a decade ago that banks must be able to aggregate risk data accurately, completely, and in a timely manner. Compliance AI that operates on data that does not meet these standards is operating outside the regulatory framework that governs the data it depends on.

Pattern 3: Third-Party AI Introducing Systemic Vulnerabilities

Regulatory accountability for the compliance function sits with the institution, not the vendor. An institution cannot satisfy a regulatory enquiry by producing the vendor’s model documentation. It must produce evidence that the model was validated by the institution against its own risk appetite, governance framework, and regulatory obligations – that the institution assessed the model and embedded the oversight mechanisms its use requires.

Pattern 4: Shadow AI in the Compliance Function

Compliance teams under resource pressure are precisely the teams most likely to adopt accessible AI tools without governance review. Compliance analysts using public LLMs to summarise regulatory guidance. Risk teams using AI-assisted search to supplement primary screening systems. Each instance creates AI use in a regulated compliance context that has not been validated, assessed for bias, or subject to model risk management review.

REGULATORY REALITY

Regulators reviewing a bank’s compliance programme do not restrict their examination to officially sanctioned systems. They examine the outputs of the compliance function and the process by which those outputs were produced. An AI-assisted output the institution cannot account for is an output it cannot defend.

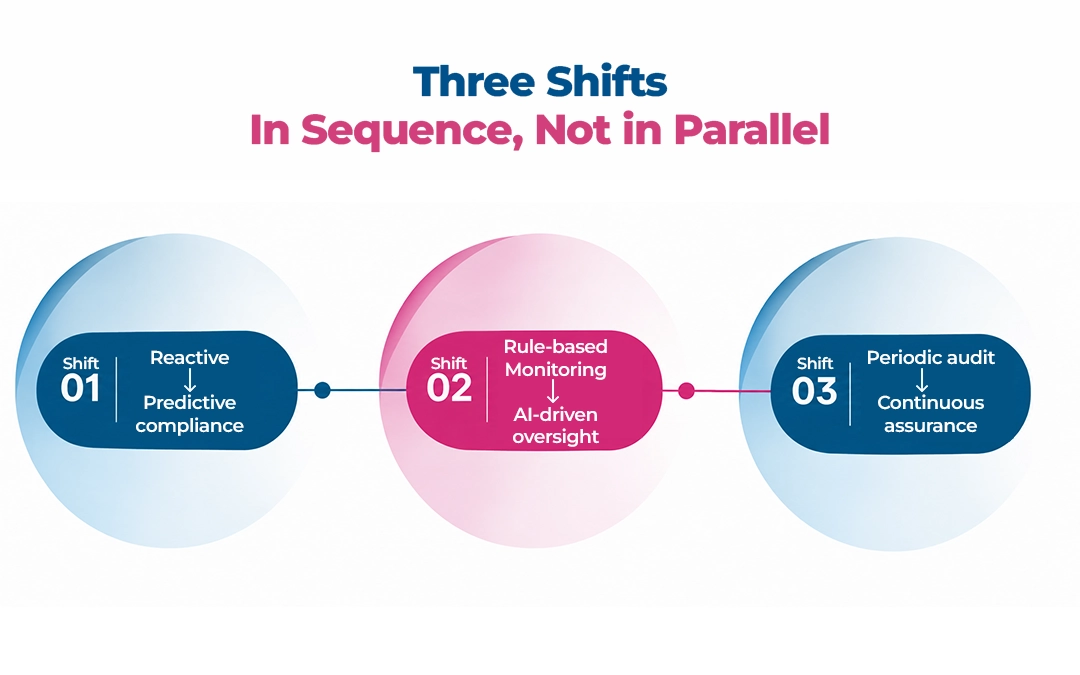

Three Shifts – In Sequence, Not in Parallel

The path to compliance assurance requires three specific shifts. The sequencing is not optional – the second builds on the first, the third requires the second.

Shift 1 (First): From Reactive to Predictive Compliance

Reactive compliance identifies failures after they have occurred. In an AI-driven compliance system where failures can propagate at the speed of real-time operations, reactive compliance is structurally inadequate. By the time a failure is reactive-detectable, it has typically accumulated across enough decisions to constitute a material compliance event.

Predictive compliance monitors the leading indicators of compliance failure before it occurs: model performance trending toward thresholds that historically precede accuracy degradation, data quality metrics trending toward levels that precede compliance output errors.

What it requires: compliance performance dashboards monitoring model behaviour, data quality, and decision consistency in real time – not monthly reports, but live operational intelligence that the compliance function owns and acts on daily. This shift comes first because it provides the visibility that the subsequent shifts depend on.

Shift 2 (Second): From Rule-Based Monitoring to AI-Driven Oversight

Rule-based compliance monitoring applies fixed criteria – deterministic, auditable, consistent, and static. AI-driven compliance oversight applies adaptive intelligence that detects anomalies across complex, multi-dimensional transaction data that rule-based systems cannot represent.

The governance challenge: the explainability gap that adaptive oversight introduces. What it requires: explainability infrastructure built into the AI oversight system at the point of design – the ability to produce a coherent account of why a specific transaction was flagged, in the format that satisfies the examination standard, within the timeframe the regulator specifies. For AML, this means a SAR narrative the compliance officer can review, validate, and sign off on – not a model confidence score.

Shift 3 (Third): From Periodic Audit to Continuous Assurance

The audit cycle that governs most banking compliance programmes was designed for rule-based systems: periodic review, annual model validation, quarterly risk assessment. AI-driven compliance systems do not hold still between audits. Models drift. Data quality changes. New transaction typologies emerge.

Continuous assurance means the compliance function’s AI estate is subject to ongoing automated monitoring providing the equivalent of an audit-ready state at all times – not a preparation exercise before an examination, but a permanent operational posture. What it requires: compliance governance framework redesigned for the operating cadence of AI – shared live operational view, model risk management incorporating ongoing production performance data, compliance leadership treating AI governance as a core operational competency.

What Regulators Are Examining Now – and What Is Coming Next

The current examination standard: can the institution demonstrate that its compliance AI was validated before deployment, that model risk management processes were applied, that explainability frameworks exist, and that oversight mechanisms are in place? This is essentially an SR 11-7 standard applied to AI.

The next phase – already visible in Federal Reserve guidance, the EU AI Act, and FCA Consumer Duty implementation – will examine whether governance is operational, not just documented. Whether the monitoring infrastructure is actually being used. Whether the institution can demonstrate, with evidence from production data, that its compliance AI is performing within governance parameters.

The distinction between governance as documentation and governance as operational practice is the distinction that will separate institutions that pass the next phase from those that do not.

In AI-first banking, compliance is not the boundary of what AI can do. It is the standard that everything AI does must be able to meet. The institutions that close the assurance gap proactively will not just pass the examination. They will define what the standard looks like.

This article is part of the Engineering Trust in AI-First Banking series, examining the framework that separates institutions that scale AI from those that stall.

The full research report examines AI-in-compliance in the context of the Four-Layer Trust Architecture – showing how data trust, model trust, system trust, and outcome trust apply specifically to the compliance function, and what each of the three shifts requires across all four layers.

Download the Full Research Report: Engineering Trust in AI-First Banking

What to Read Next

PREVIOUS: AI-Enabled Core Banking: Re-Architecting the Foundation for Intelligence

NEXT: The Market Gap: AI Capability vs Execution Confidence – the market-level verdict

FAQ

1. What is the difference between compliance automation and compliance assurance in AI-first banking?

Compliance automation means using AI to execute compliance tasks – transaction monitoring, regulatory reporting, KYC screening – faster and at greater scale than human teams. Compliance assurance means those automated processes produce outcomes that are consistently accurate, explainable, auditable, and defensible under regulatory examination – not just at go-live, but continuously over time. Most institutions have achieved automation. Very few have achieved assurance, and the gap between the two is where regulatory findings are concentrated.

2. What are the four compliance risk patterns that emerge specifically from AI-driven compliance systems?

The four patterns are: model bias that systematically mis-calibrates risk assessments across customer segments; data quality failures that cause compliance AI to process decisions on inputs that do not reflect current customer or transaction state; explainability gaps that prevent institutions from reconstructing why specific decisions were made; and governance velocity mismatch where compliance AI models are updated faster than the oversight frameworks reviewing them. Each pattern individually is manageable; they typically compound together in practice.

3. How are regulators changing their approach to AI governance in compliance functions?

Regulators are shifting from watching AI adoption to actively examining AI governance. The EU AI Act classifies credit scoring and AML monitoring as high-risk. The OCC, Federal Reserve, and CFPB have all signalled that explainability and transparency in AI-driven compliance decisions are not architectural preferences – they are compliance requirements. The practical implication: a compliance AI system that cannot produce an explanation for an individual adverse action or suspicious activity determination is not compliant, regardless of its aggregate accuracy.

4. What are the three sequenced shifts that move a bank from compliance automation to compliance assurance?

The three shifts are: from retrospective review to predictive compliance monitoring (using AI to identify anomalies before they become violations, not after); from output auditing to AI-driven oversight with explainability at the determination level (ensuring every compliance decision carries a re-constructable rationale, not just a result); and from periodic governance to continuous assurance as an operational posture (where compliance AI is monitored, validated, and evidenced in real time, not prepared for examination). These must be sequenced – the third shift requires the second, and the second requires the first.

5. Can AI actually reduce regulatory risk in banking, or does it introduce more risk than it removes?

AI reduces regulatory risk when deployed with adequate governance infrastructure – specifically when it can detect patterns at a scale and speed human teams cannot match, and when the decisions it makes are explainable and auditable. It increases regulatory risk when deployed without that infrastructure, because it makes consequential decisions at a volume that makes retrospective review structurally impossible. The honest answer is that AI’s impact on regulatory risk in banking is determined almost entirely by the governance architecture around it, not by the AI capability itself.