Why This Article Matters

Generative AI is not a more capable version of traditional AI. It is a different risk class – and the governance frameworks most institutions have built for traditional AI are not designed for it. This article makes the critical distinction that most GenAI governance discussions miss: traditional AI trust is built on validating outputs, but GenAI trust requires governing behaviour. These require different architectures, different ownership models, and different evaluation criteria. It also includes the most practically useful content in this series: a specific list of banking decisions that GenAI must never make as the final decisioning layer – and why. If you are deploying or evaluating GenAI in a regulated banking context, this is required reading.

Within eighteen months of large language models becoming enterprise-deployable, banks were running GenAI across customer service chatbots, document processing pipelines, regulatory reporting workflows, relationship manager assistants, and compliance monitoring systems. The deployment velocity was extraordinary. The governance frameworks evolving to contain it were not.

The result is an emerging risk profile that is genuinely distinct from the AI risk the industry has been managing for the past decade. And it requires a trust model that most institutions have not yet built.

Traditional AI trust = validate outputs. GenAI trust = govern behaviour. These require different architectures.

Traditional AI models are deterministic within their decision space: given the same inputs and model state, they produce the same output. This determinism is what makes traditional AI auditable.

Generative AI models are probabilistic across an effectively infinite output space: given the same input, they can produce meaningfully different outputs depending on model state, temperature settings, context window content, and stochastic sampling processes. In a non-regulated industry, this variability is manageable. In banking – where customer communications carry legal weight, product information must be accurate, and credit decisions carry regulatory obligations – that variability is a structural liability.

And it stress-tests all four layers of the Trust Architecture simultaneously: data trust is stressed by untraceable information surfacing, model trust is stressed by the irreducible explainability gap, system trust is stressed by context-sensitivity that makes environment consistency structurally harder to achieve, and outcome trust is stressed by the verification burden on GenAI outputs.

Five Risk Surfaces Specific to GenAI in Banking

Risk Surface 1: Hallucination in Customer-Facing and Operational Contexts

The danger of hallucination in banking is not that it is dramatic or obvious. It is that it is neither. Hallucinations in well-designed GenAI systems are typically fluent, contextually appropriate, and confidently delivered – indistinguishable from correct outputs to the customer receiving them and in many cases to the internal reviewers monitoring them.

A GenAI-powered customer service assistant provides a customer with incorrect information about early repayment charges on their mortgage product – because the retrieval layer that was supposed to surface current product terms failed silently. The customer makes a financial decision based on that information. The FCA’s Consumer Duty – which requires communications to be clear, fair, and not misleading – applies regardless of whether the communication was written by a human or generated by an AI.

Risk Surface 2: Explainability Deficit in Regulated Decision Contexts

Traditional AI explainability is challenging but tractable. The mechanisms exist – SHAP values, attention attribution, decision tracing. GenAI explainability is a different problem. The output of a large language model emerges from token-by-token probabilistic sampling across billions of parameters. There is no ‘feature’ that can be attributed a weight in the same sense a gradient boosting model feature can.

This creates a specific constraint: there are decision contexts in which GenAI should not be used as a direct decisioning tool – not because the output is likely to be wrong, but because the institution cannot satisfy the explanation obligation that the decision context carries.

Risk Surface 3: Data Leakage and Privacy Exposure

In retrieval-augmented GenAI architectures – the most common enterprise deployment pattern – the risk is operational and continuous. If access controls on the retrieval layer are not granular and correctly implemented, the system can surface information about one customer in a context where that information has not been authorised – because the retrieval is based on semantic similarity, not on access permissions. Under GDPR Article 22 and its banking-specific applications, this can create a data protection incident with regulatory notification obligations.

Risk Surface 4: Behavioural Inconsistency Across Channels

A bank deploys a GenAI-powered product explanation capability across its digital channel, its contact centre agent assist tool, and its branch advisor support system. All three are powered by the same underlying model. But the system prompt is slightly different in each context, the retrieval layer is configured differently, and the model version has been updated in the digital channel but not yet propagated to the contact centre. Customers asking the same question across different channels receive responses that are consistent in substance but different in specifics – different fee figures, different eligibility criteria. Under fair treatment obligations, this is not a systems architecture problem. It is a customer harm problem.

Risk Surface 5: Shadow AI and the Uncontrolled Adoption Problem

Of the five risk surfaces, this is the one most consistently underestimated by senior technology leaders – and the one most likely to produce the regulatory finding that causes the largest programme disruption.

Compliance teams using consumer LLMs to summarise regulatory guidance. Collections teams using AI-generated communications that have not been reviewed for fair treatment compliance. Risk teams using AI-generated analysis in board briefings. None of this is malicious – it is the predictable result of a capability gap. In the EU, the AI Act’s requirements for transparency and human oversight apply to AI that is in operational use, not just formally approved. Regulators do not accept ‘we didn’t know the business team was using it’ as a governance defence.

GenAI Decisions That Must Not Be Made by AI Alone

The most practically useful guidance for a CIO governing GenAI in a regulated banking environment is not a list of what GenAI can do. It is a list of what GenAI must not be the final decisioning layer for:

- Credit and lending decisions with adverse action obligations: – GenAI can support the process but the decision-level explainability required under ECOA, the Consumer Credit Directive, or equivalent frameworks cannot be reliably produced from probabilistic text generation

- Collections communications that carry fair treatment obligations: – consistency across comparable customers and traceability to specific input conditions are requirements that GenAI architecture cannot currently guarantee at scale

- AML and financial crime escalation decisions: – the decision to file a Suspicious Activity Report carries legal weight and regulatory obligations that cannot be delegated to a system whose reasoning cannot be reconstructed

- Regulatory submissions and board-level risk reporting: – any document formally submitted to a regulator requires authorship accountability that GenAI cannot provide

- Customer-specific financial advice in regulated advice contexts: – where suitability assessment, disclosure, and audit trail requirements apply, AI-generated advice that cannot satisfy this standard is unauthorised advice

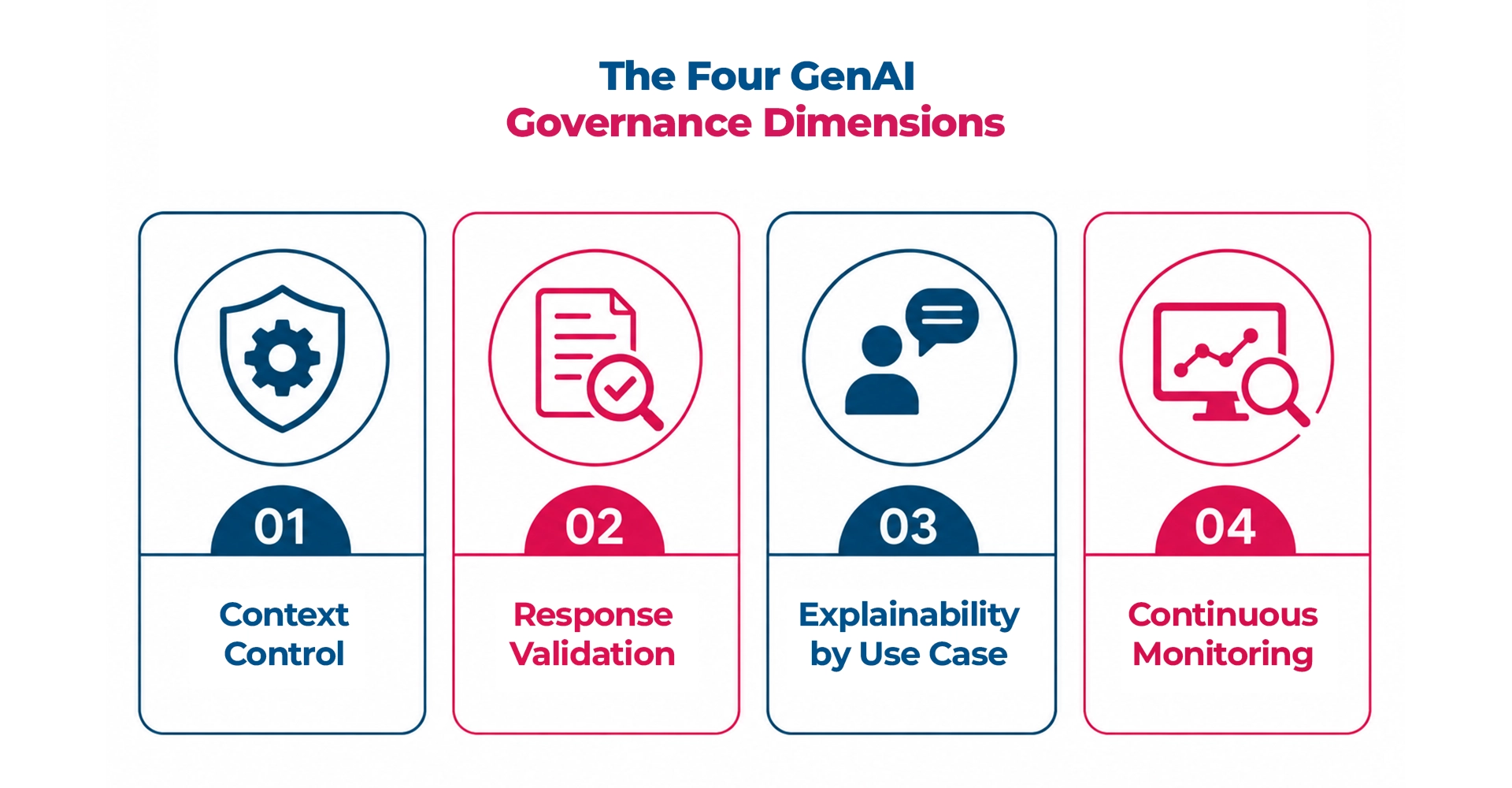

The Four GenAI Governance Dimensions

- Context Control: – system prompts as governed artefacts, version-controlled and consistently deployed across every context. Retrieval layers that enforce data access at the semantic level. Explicit out-of-scope routing.

- Response Validation: – automated screening of generated outputs against factual accuracy checks and regulatory compliance rules before delivery. Confidence scoring. Anomaly detection on output distributions.

- Explainability by Use Case: – a taxonomy of which decisions require decision-level explanation, which require process documentation, and which require human sign-off with GenAI as supporting analysis only.

- Continuous Monitoring: – a GenAI deployment register covering unsanctioned deployments, usage monitoring across the full operational footprint, and red-teaming exercises that systematically probe production GenAI boundaries.

Generative AI will define the next phase of AI-first banking. The question is not whether to deploy it. The question is whether the institution has built the governance architecture that makes deployment an advantage rather than an accumulating liability.

GenAI governance is examined in the context of the full Four-Layer Trust Architecture in the complete research report – showing how each GenAI risk surface maps to a specific trust layer and what the governance response at each layer requires.

Download the Full Research Report: Engineering Trust in AI-First Banking

What To Read Next

PREVIOUS: From Adoption to Outcome Assurance: The AI Maturity Spectrum

NEXT: AI Banking Solutions: Capability Without Trust Does Not Scale – the vendor evaluation framework

This article is part of the Engineering Trust in AI-First Banking series, examining the framework that separates institutions that scale AI from those that stall.

FAQ

1. Why is generative AI in banking considered a different risk class from predictive AI?

Predictive AI produces a specific output – a credit score, a fraud flag, a risk rating – for which attribution and validation are well-understood. Generative AI produces open-ended content, reasoning, and recommendations at scale, with outputs that are harder to validate systematically and where errors can propagate in ways that are difficult to detect before they become consequential. In banking, where outputs influence customer communications, regulatory filings, credit decisions, and operational workflows, the combination of scale and unpredictability creates governance obligations that standard model risk frameworks were not designed to address.

2. What are the five risk surfaces specific to generative AI in banking?

The five risk surfaces are: hallucination risk (where models produce confident but factually incorrect outputs); data leakage risk (where model interactions expose confidential customer or institutional data); compliance risk (where generated content or recommendations violate regulatory obligations without triggering standard controls); attribution risk (where it is unclear which model version or input produced a specific output); and concentration risk (where dependence on a single model provider creates systemic exposure across multiple banking functions simultaneously).

3. What decisions should generative AI never make as the final decisioning layer in a bank?

Generative AI should not be the final decisioning layer for any outcome that carries direct customer impact, regulatory obligation, or financial consequence without human oversight – including adverse credit decisions, suspicious activity reports, regulatory communications, and customer-facing determinations that trigger legal rights. These require explainability standards, audit trails, and accountability structures that generative AI, as currently governed, cannot reliably satisfy at scale in a regulated banking environment.

4. How should banks structure governance for generative AI that is already in production use?

Governance for deployed generative AI in banking requires four dimensions: use case classification (which applications carry high-risk regulatory obligations versus low-risk productivity use); output validation (systematic review mechanisms that catch hallucinations and compliance violations before they reach customers or regulators); data boundary enforcement (technical controls that prevent model interactions from exposing protected data); and model change management (version control and impact assessment for model updates that affect production outputs). Institutions that retrofitted governance after deployment consistently report higher remediation costs than those that established these dimensions before going live.

5. Is generative AI in banking mature enough to use in customer-facing applications?

Generative AI can be used responsibly in customer-facing applications when bounded appropriately – specifically, when outputs are constrained to defined, validated response patterns and when human review mechanisms are in place for edge cases. Unbounded conversational AI in contexts involving financial advice, credit guidance, or account decisions is not yet at the governance maturity level that regulatory obligations in banking require. The practical answer is: yes, with well-defined scope and oversight architecture; no, as an unconstrained decision-making interface.