Why This Article Matters

The CIO’s mandate in banking has not just become harder – it has become structurally different. In the digital-first era, success was measured by whether systems functioned. In the AI-first era, the CIO is accountable for whether the decisions those systems make are reliable, explainable, and defensible. That is a governance accountability for machine-made decisions at enterprise scale – and it changes what every one of the four core imperatives actually requires. This article examines each imperative precisely: the opportunity, the failure mode, and why trust infrastructure is not a constraint on any of them but the load-bearing condition beneath all four.

What Has Actually Changed at the CIO Level

In a digital-first bank, the CIO’s primary obligation is delivery: build systems that function, deploy them reliably, maintain the operational stability of the technology estate. Success is largely technical – did the system launch, does it perform, is it available?

In an AI-first bank, the obligation is different in a way that matters enormously. The CIO is now accountable not just for whether the system works – but for whether the decisions the system makes are reliable, explainable, and defensible. This is a fundamentally different standard.

A traditional system that processes a transaction either completes it or fails. An AI system that makes a credit decision, flags a fraud event, or personalises a customer interaction is exercising judgment at scale, on behalf of the institution, under regulatory scrutiny, and in ways that directly affect the financial lives of customers. The accountability that follows is not just technical. It is governance accountability – for the quality of machine-made decisions at enterprise scale.

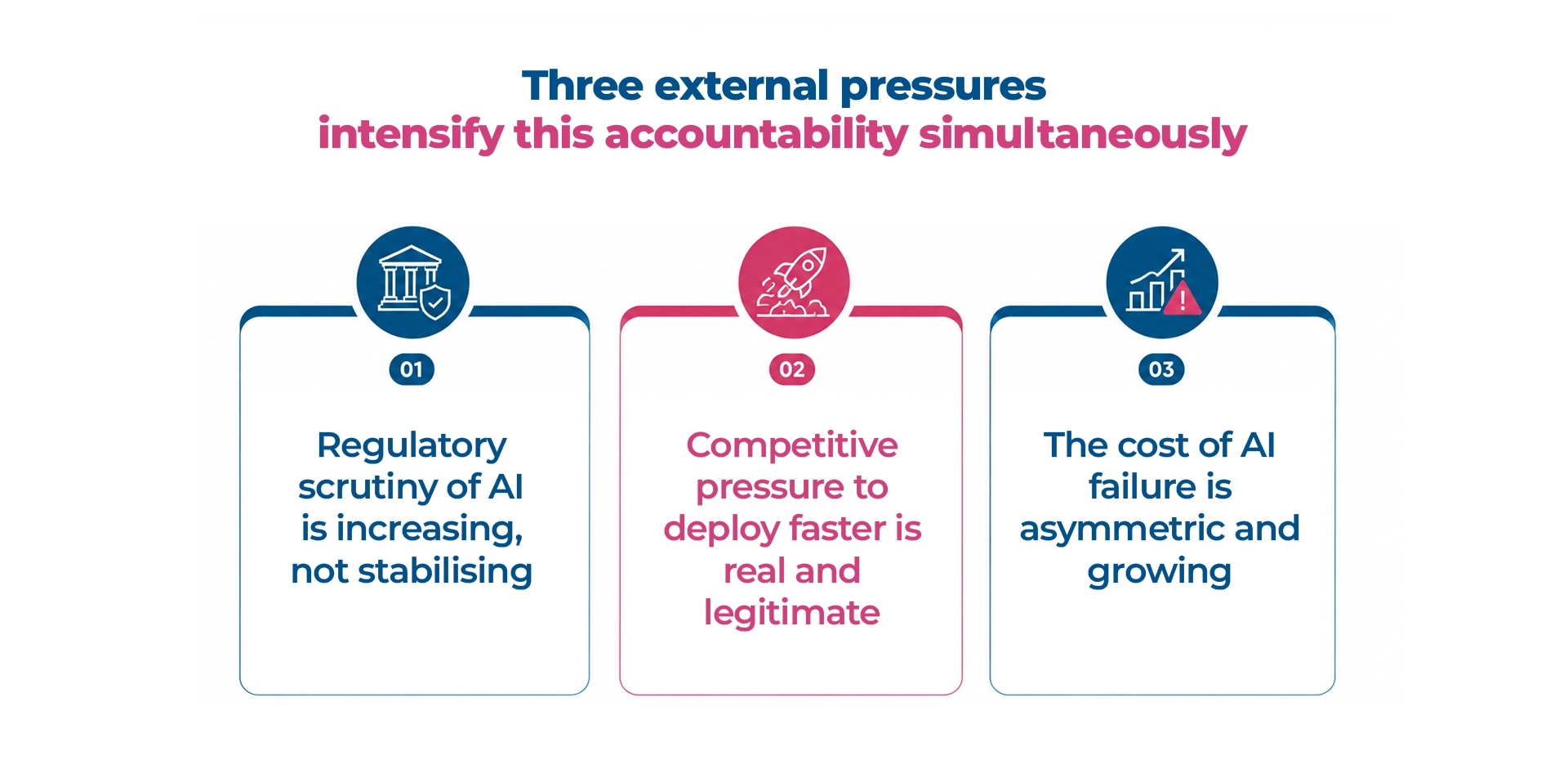

Three external pressures intensify this accountability simultaneously:

- Regulatory scrutiny of AI is increasing, not stabilising: – the EU AI Act, Federal Reserve and OCC guidance on model risk, CFPB enforcement on algorithmic credit decisions. Regulators are moving from watching AI adoption to examining AI governance.

- Competitive pressure to deploy faster is real and legitimate: – digital-native challengers, embedded finance platforms, and tech-enabled providers are not constrained by legacy infrastructure or organisational complexity.

- The cost of AI failure is asymmetric and growing: – a failed AI deployment in 2025 is simultaneously a customer harm event, a regulatory exposure, a brand event, and a financial loss. Often in the same news cycle.

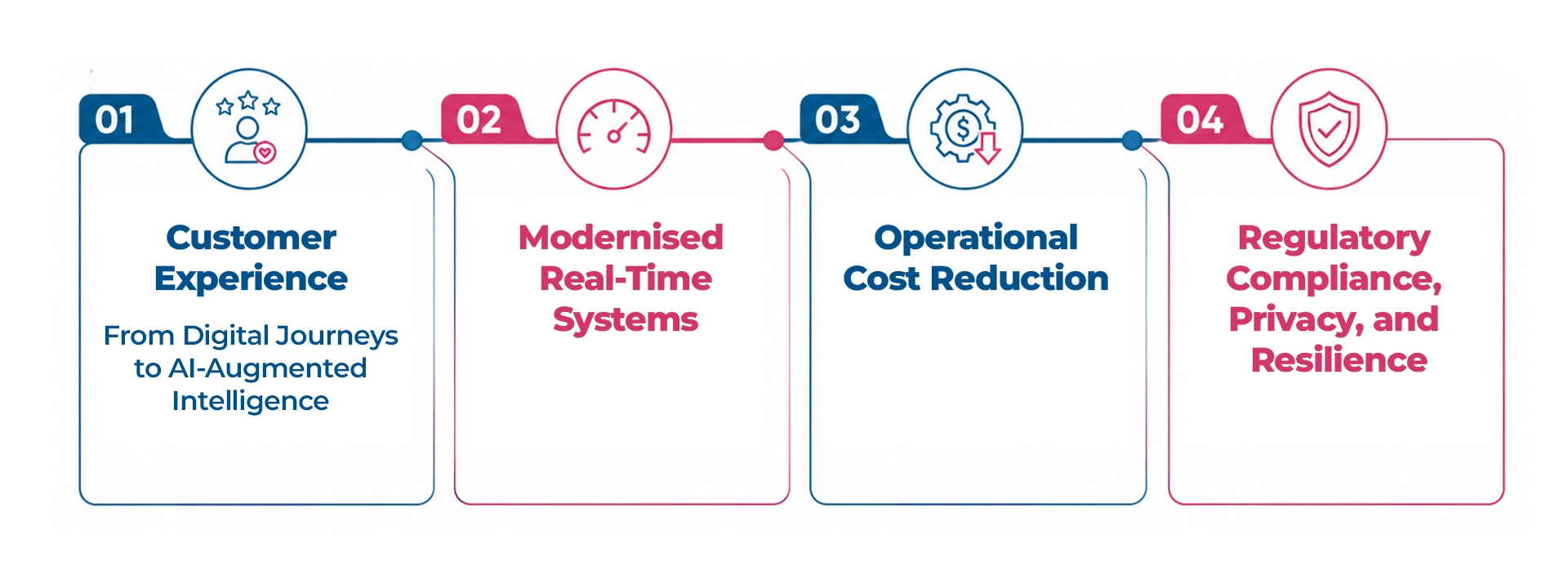

Imperative 1: Customer Experience – From Digital Journeys to AI-Augmented Intelligence

The mandate operates across three connected dimensions: AI-augmented onboarding and customer service, real-time customer segmentation and hyper-personalisation, and faster release of digital products.

The opportunity is clear and well-documented. What is consistently underestimated is the failure mode: an AI-driven personalisation engine on inconsistent customer data across channels does not deliver personalised experience. It delivers contradictory experience – different offers, different risk assessments, different communications reaching the same customer from systems that do not share a coherent view of that customer. The AI is functioning. The outcome is incoherence. The customer experiences not personalisation but inconsistency.

The CIO’s challenge is not whether to pursue AI-driven customer experience transformation. It is how to build the data foundations, governance frameworks, and continuous validation infrastructure that allow it to deliver what it promises.

How AI is moving customer onboarding from self-service to zero-service – and what a multimodal customer engagement architecture looks like at enterprise scale: From Digital-First to AI-First: The CIO’s Customer Experience Mandate

Imperative 2: Modernised Real-Time Systems

Core banking systems were engineered for transaction accuracy, data integrity, and operational stability under high volume. They were not engineered for real-time decisioning, continuous data streaming, probabilistic model integration, or the API-first composability that AI-native architectures require.

The failure mode is specific: a core that has been modernised for speed without resolving its data governance deficit is not more reliable. It is faster and more fragile – propagating data inconsistencies at real-time velocity rather than managing them within a batch cycle. This is where data governance becomes a prominent, load-bearing dependency – not a background programme, but the foundational discipline without which core modernisation delivers faster fragility instead of trusted intelligence.

The architectural shift from systems of record to systems of intelligence – event-driven design, composable cores, and what data contracts look like in a live AI-enabled core banking environment: The CIO’s Guide to AI-Enabled Core Banking Modernisation

Imperative 3: Operational Cost Reduction

The promise of AI-led automation across customer service, lending operations, payments processing, fraud investigation, and compliance monitoring is one of the most compelling value propositions in the AI-first transition. The efficiency gains are real. But they are only real when the automation operates on a foundation of reliable data and continuous validation.

Automation that processes decisions at scale on unreliable data does not reduce operational cost. It amplifies operational risk – because every automated decision carries the same compliance obligations and customer impact as a human decision, but at a volume and velocity that makes manual oversight structurally impossible. A fraud detection system generating false positives at scale is not a cost reduction. It is a customer experience failure and an operational overhead simultaneously.

How AI-led automation is transforming banking cost structures – and why efficiency gains require validation infrastructure to be real rather than deferred liabilities: Engineering Trusted Automation in AI-First Banking Operations

Imperative 4: Regulatory Compliance, Privacy, and Resilience

Of the four imperatives, this is the one where the window for preparation is narrowing most rapidly – and where the cost of unpreparedness is highest. The EU AI Act classifies credit scoring, AML monitoring, and other AI applications in financial services as high-risk. The Federal Reserve and OCC have signalled increasing supervisory focus on AI governance. The CFPB has moved from guidance to enforcement on algorithmic decision-making.

Regulators are no longer watching AI adoption. They are examining AI governance. The question is not whether an institution is using AI. It is whether the institution can demonstrate that its AI is controlled, explainable, aligned with customer obligations, and auditable when something goes wrong.

Data governance is the foundation of every regulatory obligation in AI banking. A bank cannot produce an accurate adverse action notice for a credit decision made by a model trained on unreliable data. It cannot demonstrate model fairness when the training data contains unresolved demographic biases. It cannot satisfy a BCBS 239 examination when the data feeding its AI risk models is inconsistently governed.

How AI-first banks are moving from periodic audit to continuous compliance assurance – with explainability and auditability as architectural requirements: Engineering Trust in AI Compliance and Regulatory Governance

The Condition That Runs Through All Four

Each imperative fails – in documented practice, across institutions of every tier – when pursued without the infrastructure to generate sustained confidence in the systems being built.

Customer experience AI fails when data inconsistency produces contradictory personalisation. Core modernisation fails when the new architecture is faster but built on unresolved data governance debt. Automation fails when the volume of AI-driven decisions outpaces the validation infrastructure that makes them defensible. Regulatory compliance fails when governance frameworks are not designed to travel at the speed of AI deployment.

The common thread is not a technology gap. It is a trust infrastructure gap. And this is the precise point at which the CIO’s mandate becomes its most demanding – and its most consequential.

The CIO who builds trust infrastructure not as a control layer above the four imperatives but as the engineering foundation beneath them is not adding friction to transformation. They are building the only structure on which genuine AI-first scale is possible.

The complete framework – what trust infrastructure means architecturally, how the four-layer trust architecture maps to each imperative, and the maturity spectrum that shows where your institution stands – is available in the full research report.

Read the Full Framework: Engineering Trust in AI-First Banking

This blog is part of the series: Engineering Trust in AI-First Banking

What to Read Next

PREVIOUS: Speed Without Trust Creates Risk – the four execution failure patterns and the trust layer architecture

NEXT: What Trust Means in AI-First Banking – the Four-Layer Trust Architecture defined precisely

FAQ

1. What are the four core imperatives that define the CIO’s mandate in AI-first banking?

The four imperatives are:

- Customer engagement and growth (AI-augmented onboarding, hyper-personalisation, faster product release),

- Infrastructure and application modernisation (AI-native cloud platforms, API-first architecture, real-time systems for lending, deposits and payments),

- Operational cost reduction (AI-led automation across customer service, fraud, and compliance) and

- Regulatory compliance, resilience and privacy (continuous governance, predict-prevent-mitigate-recover-restore frameworks).

None of these can be pursued in isolation and each fails without a common foundation of engineered trust.

2. Why is data governance described as the thread that runs through all four CIO imperatives?

Because every imperative depends on the quality, consistency, and auditability of the data that feeds its AI systems. Customer personalisation fails on inconsistent customer data. Modernisation propagates fragility faster if data governance debt is unresolved. Operations automation amplifies risk when processing decisions on unreliable inputs. Regulatory compliance becomes indefensible when the data underlying AI decisions cannot be traced and validated. Data governance is not one of the four imperatives – it is the condition beneath all of them.

3. How is the CIO’s accountability in AI-first banking structurally different from the digital-first era?

In the digital-first era, success was largely technical: did the system launch, perform, and stay available? In the AI-first era, the CIO is accountable for whether machine-made decisions – at scale, in real time, affecting customers and carrying regulatory obligations – are reliable, explainable, and defensible. That accountability does not wait for the governance framework to catch up. It exists from the moment AI is in production making consequential decisions.

4. What does “trust infrastructure as the load-bearing foundation” mean in practice?

It means that the Four-Layer Trust Architecture – continuous validation, data integrity, explainability, and integrated governance – is not a control layer sitting above the four imperatives. It is the engineering foundation without which each imperative degrades: faster delivery without validation produces unreliable releases; modernised infrastructure without data governance produces faster fragility; automated operations without reliable data amplifies risk; and compliance AI without governance accumulates regulatory exposure. Trust infrastructure is what holds the four imperatives up.

5. How should a CIO prioritise across the four imperatives when resources and time are constrained?

The practical answer is to sequence by dependency rather than by business priority. Data governance and continuous validation infrastructure should be established first, because they underpin all four imperatives. Customer experience and modernisation initiatives can then proceed with confidence that the foundation is sound. Operations automation and compliance assurance build on that foundation. CIOs who sequence by business priority alone – starting with the highest-visibility imperative – typically discover that their transformation programmes plateau or fail at the point where trust infrastructure would have been needed.